Marcellus shale gas well, Pennsylvania-photo WCN 24-7

We have seen a spate of think tank publications and opinion pieces doubting the economic and geological potential of shale gas in Europe. According to Nick Grealy, these are all based on outdated statistics and overly conservative assumptions. The US example shows shale gas resources are much larger than the sceptics claim. There is really only one obstacle to exploiting Europe’s shale gas potential: we don’t want it in our backyard. But then do we want the Russians there instead?

A consistent motif among European shale fractivists and their City of Londongrad energy advisers/enablers has been that US shale production is too good to be true and will either disappear completely or be incredibly expensive after some declines that are just around the corner. Paul Stevens of Chatham House, Mike Liebreich of Bloomberg New Energy Finance (BNEF), and John Dizard of the FT are all promoters of the theory that if US shale gas is a chimera, European and UK shale gas will, by extension be an even more expensive delusion. Let’s just call the whole thing off and keep on investing in renewables is one angle, although keep on buying Russian gas is an important subtext. The logic there is that Russia’s huge resources will always be the most reliable and cheaper in the long term. That theory has obviously gone bang big time, but how about the decline theory?

Faith in the shale fail theories is the final death rattle of the Peak Oil tendency. A key part of Peak Oil is to blind people not with science but with yesterday’s statistics. Models and scenarios are built on data from the past. Stevens, BNEF and Dizard miss one of the fundamental points of the shale revolution: the future won’t simply be a continuation of the past. The improvements in efficiency mean that, as even shale skeptic in chief Art Berman himself put it last year in a Houston presentation, anything over 45 days in shale gas is ancient history.

But to the Greenpeace, Gazproms and Friends of the Earth of the world, shale is a dangerous uneconomic fantasy. That message then gets transmitted to the local level: Not only will we poison the earth, we won’t even see any economic benefit. Best to go full speed ahead on renewables, while depending on those nice Russians to keep the pipes full with a short term need for gas as the transition ramps up. Hardly worth the cost of those trucks scaring the horses for a few weeks.

The problem with that theory has been the continual rise in production. Drill rig counts go down, laterals increase, costs go down, wells per pad increase, frack stages increase and production for both oil and gas soars. Many sceptical papers don;t get this. They posit shorter laterals, single well pads, longer drill times, lower production and higher costs.

A case in point is the Marcellus: most of the statistics in sceptical publications don’t take any Marcellus figures into account since this play has really only taken off in the past two years. The shale doubters thus depend a lot on analysis of the original US shale play, the Barnett. One could say the Barnett is a far smaller play and doesn’t provide an accurate view of the future of other shales, in the US, or internationally. But a new study by the University of Texas Bureau of Economic Geology foresees a lot of life remaining even there:

- A comprehensive study of the reserve and production potential of the Barnett Shale integrates engineering, geology, and economics into a numerical model that allows for scenario testing based on several technical and economic parameters. The study was conducted by the Bureau of Economic Geology (BEG) at The University of Texas at Austin and funded by the Alfred P. Sloan Foundation.

- In its base case, the study forecasts a cumulative 45 Tcf of economically recoverable reserves from the Barnett, with production declining predictably to about 900 Bcf/year by 2030 from the current peak of about 2 Tcf/year.

- The forecast falls in the mid to higher end of other known predictions for the Barnett and suggests that it will continue to be a major contributor to U.S. natural gas production through 2030.

But the Greens and Russian gas enthusiasts don’t have a good track record of trusting geologists.They like conservative simple numbers they can understand: How much gas is there and how much will it cost. They look askance, not without some reason, at predictions from upstream exploration companies or the service industry. Any predictions of lower downstream costs are seen as wishful thinking from the likes of industrial consumers or Ineos or Tory politicians, or climate change skeptics: Choose your bogeyman.

However, if you want to be sceptical of the upstream producers and downstream consumers, let’s consider the midstream sector, the companies providing the physical infrastructure to connect the two. By definition they have to be a cautious industry. Pipelines are financed on a model of multi-year revenue streams. You don’t make much in midstream, but you do tend to make it forever. Pipelines are expensive and complex to build and need billions of investments. Japanese investors I know are especially enamoured of pipelines. They don’t mind making low single digit returns, they just want the returns to be as long lived as their pensioner customers – a long, long time. In short, midstream is by definition a long-term, conservative and cautious industry. Hyperbole simply doesn’t have a place. But what about reality?

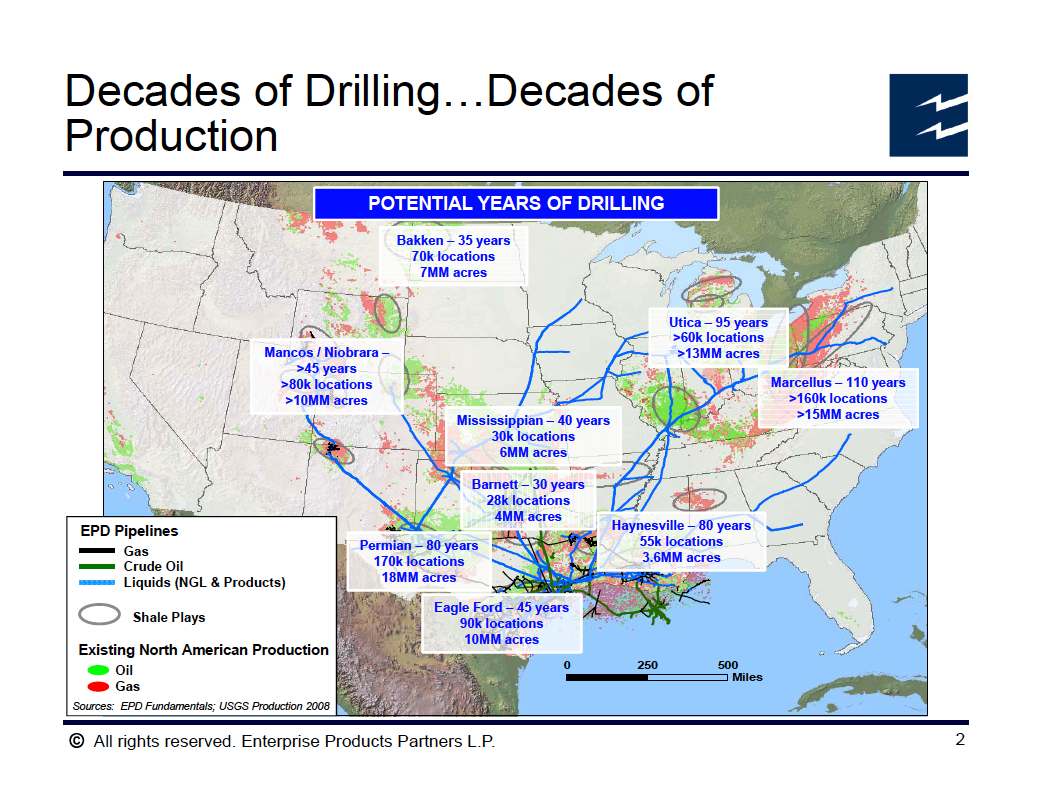

A recent presentation by Enterprise Products Partners LLP, a $64 billion US midstream transportation, storage and processing company, underlines how much things have changed. This is a case of having your cake and eating it. EPP has over 50,000 miles of pipeline, transporting not only natural gas but ethane, propane and oil.They would not be in business if they had nothing to fill them with. They could not get financing if lenders weren’t convinced the pipelines would be utilised. Be warned, the link is to a huge 176 slide presentation, but here are the key slides. The first is about how much gas is left. Decades, according to EPP, and over a century in the Marcellus.

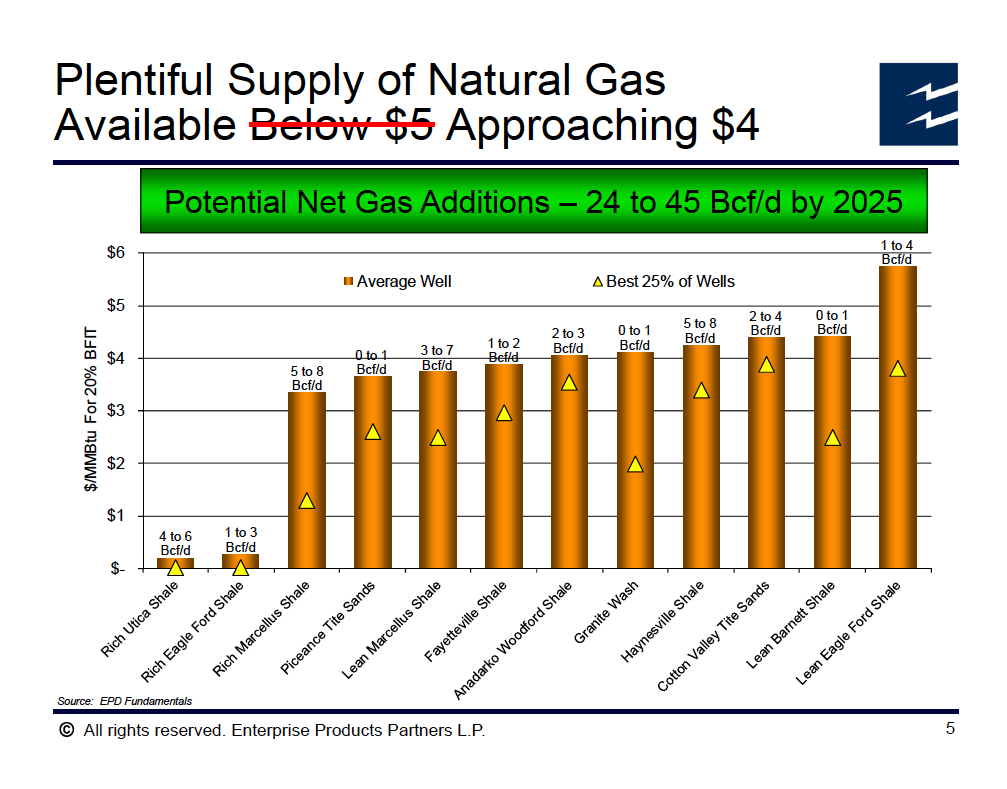

Note how much the shale economics have changed on the next slide. EPP figures contradict those given by BNEF to the House of Lords and used ever since by Greenpeace, Caroline Lucas, Friends of the Earth and WWF. BNEF says they stand by their figures, but they are for clients only and refuse to release any details. They predict that UK shale gas will be prohibitively expensive based entirely on US analogues of gas cost of $5 to $6 – so let’s call the whole thing off. It’s hard to fight against secret figures. A bit like those secret frack fluids.

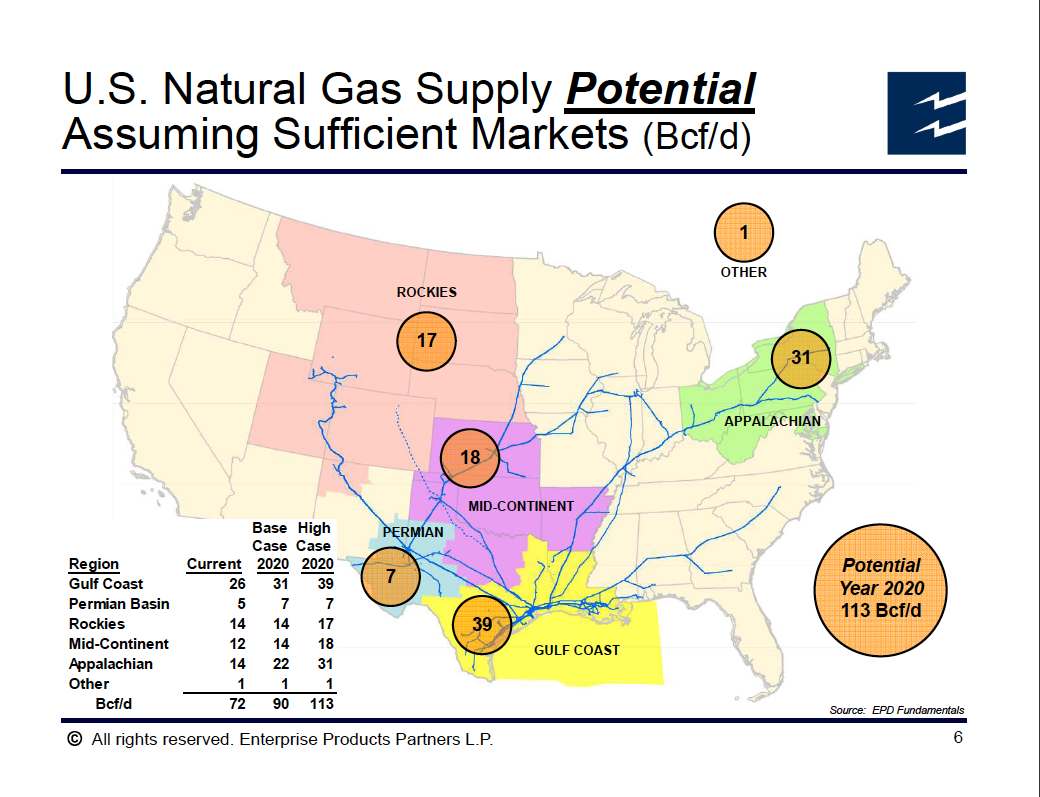

The next slide shows some mind blowing potential. At 1 BCFD (billion cubic feet per day) equal to 10.33 BCM (billion cubic metres) a year, any notion that the UK is going to struggle to hit 10 BCM by 2030 is either incredibly conservative or incredibly far fetched:

I’ve posted recently on the massive Marcellus potential, but the numbers just keep rising. Compare even the base case of 90BCFD/930BCMY to an entire EU28 consumption of only 51 BCF/525 BCMY. Much of that is coming from the Gulf Coast, primarily from the Eagle Ford and Haynesville. These numbers are almost beyond belief. Time to again underline their source, which has no interest in inflating figures. EPP are in the business of delivering first gas to customers and secondly returns to investors. There may be some strange business model of generating income by building pipelines to keep them empty, but perhaps John Dizard or Greenpeace, or Gazprom, can tell us what it might be.

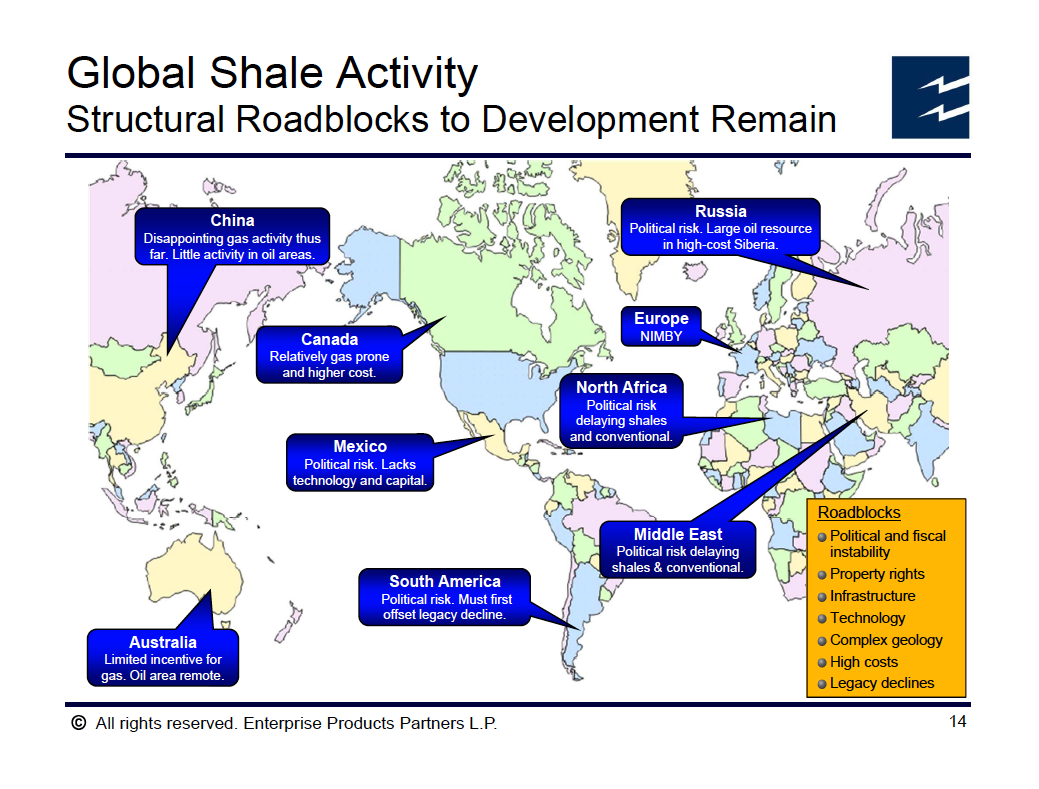

Finally, at the end of the section, EPP looked at something that might actually disrupt their model. Depending on a build-up of export infrastructure to export US shale as LNG, they naturally had to perform some competitor analysis. This is the view from Texas of shale potential worldwide:

So the real reason for Europe’s potentially disappointing potential is so simple that EPP can put it in one pathetic word: NIMBY.That however, was prior to Gazprom’s security arm jumping the shark.Thanks to that, NIMBY may be another outdated concept soon consigned to the dustbin of history.

About the author

Nick Grealy is director of the energy consultancy No Hot Air, specialising in “public perception and acceptance issues of shale energy worldwide”. Describing himself as a “recovering energy consultant” who thinks the worst energy risk is getting talked into thinking you have one, he started following the shale energy revolution in 2008. First studying what he called at the time shale’s sudden emergence and future permanence he now studies shale’s impact worldwide across the energy spectrum. He has worked for private and public clients across Europe and is a frequent contributor to media while continuing to publish analysis of energy acceptance issues at www.nohotair.co.uk This article was first published on his website here and is republished with permission from the author. All rights reserved.

Jeffrey Michel asked me to post this comment:

This is an extremely valuable article with regard to the update it provides on US shale gas prospects. Apart from that, however, it could scarcely be quoted in an academic context. The extremely complex fracking controversies being conducted in Polish, German, and French cannot be summarized by a single English acronym NIMBY. Sound geological appraisals that have already led to the rejection of CO2 storage would equally apply to particular effects of shale gas exploitation. Considerably more diligence is likewise necessary for analyzing the differences between US and European mining law. Would American property owners and communities be equally enthusiastic about fracking if they were deprived of all royalty income from gas production? Would a shale gas exploration license be imaginable for the 150 square kilometer area of the Bronx in New York City? That is precisely the situation with which we are already confronted within the city limits of Hamburg. As shown under the link http://www.volksmeter.de/Abhandlungen/HamburgSchiefergas.pdf many passages of the corresponding exploration license granted to ExxonMobil have been withheld from public scrutiny. If this corporation is trustworthy, how has it influenced the city administration to disregard the precept of information transparency? Opening Germany to shale gas development might ultimately just establish another level of corruption for which the energy industry has already gained an international reputation.