Shale gas production at Marcellus in the US by Shell – photo WCN247

A new report from the international consultancy IHS shows that the German Energiewende could still be achieved at reasonable cost if Germany were to allow domestic shale gas production. According to Nick Grealy, the IHS report offers, perhaps for the first time, a realistic, achievable strategy to make the energy transition work.

Daniel Yergin’s IHS is just about the most influential energy research house going. Yergin parlayed his talents as academic into a 1992 book “The Prize”, proving how on energy fundamentals he and his associates are the smartest guys in the room. IHS’s reputation is such that even those who rarely think about energy call on his opinion first, and take it very seriously when they hear it.

This underlines how much influence IHS’s report on German power “A More Competitive Energiewende” released on February 27 is going to have throughout Europe – and beyond – for several key reasons.

This could be the first turning of the spade on burying the energiewende dream. Or it could be the foundation for a pragmatic, optimistic, realisitic and deliverable view of the future

The energiewende, or energy transformation, has been such a totemic vision of the future to greens worldwide that the word has almost seamlessly made the leap to everyday English language. The energiewende is brandished as an example of not only the noble aims of renewable energy, but how they can, albeit with substantial initial government intervention, show a path towards a world where industrial society and renewables can co-exist. It’s cited as template for similar transitions in areas as different as the UK (Zero Carbon Britain), a Stanford study on powering New York entirely with zero carbon energy, and even a WWF study that proposes the same thing for China.

Ripple out

The IHS report is equally groundbreaking, if not downright earth-shaking. This could be the first turning of the spade on burying the energiewende dream. Or it could be the foundation for a pragmatic, optimistic, realistic and deliverable view of the future.

Here are the key IHS findings:

- The energiewende is not achieving any of its trilemma purposes of reducing carbon, increasing energy security or ensuring affordability.

- Fixing the energiewende involves the clear addition not only of natural gas, but of German shale gas.

- Accessing shale gas in Germany, Europe’s largest consumer, will lower gas prices by up to 20%.

The German impact will inevitably lower gas prices in the European wholesale gas market and will ripple out to the UK NBP (itself already tied to European prices), the second most liquid gas hub globally. European shale will thus lower gas prices not only in the UK, but via the increasing link of Henry Hub and NBP gas prices to Japanese prices, everywhere else.

The zeitgeist of the energiewende needs to move towards realpolitik

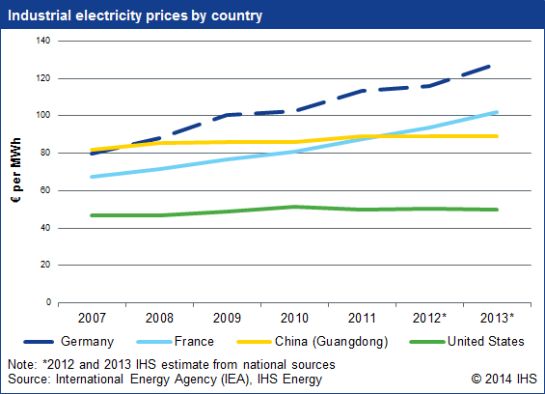

The objective of the Energiewende was a competitive transition to a low carbon economy. One of the key principles of this transition was to maintain “competitive energy prices.” Germany has rapidly developed renewables capacity, but it has not generated the expected reduction in CO2 emissions. Moreover, with some of the highest electricity prices in the industrial world, Germany has failed to achieve its competitive energy price goal.

That won’t be news to energy professionals, but it may be news to those who mistakenly cling to outdated concepts. To use more German loan words, the zeitgeist of the energiewende needs to move towards realpolitik.

IHS then goes on to the core of the argument. The study describes a path to get the Energiewende back on the course originally intended. It points the way to a “More Competitive Energiewende,” pivoting away from a focus solely on renewables development toward a more balanced approach. A more measured pace of renewables growth brings an increase in CO2 emissions over the path of the current Energiewende. However, using gas fired generation instead of coal as a complement to renewables reduces this impact in a cost-effective way.

Detailed analysis

What’s particularly important about this study is that once IHS prescribe the cure of natural gas, they then start to dose out the most obvious source of medicine.

Development of Germany’s domestic shale gas resources would allow gas to play a larger role in the power system without increasing imports. IHS performed a detailed analysis of Germany’s shale gas potential to better understand this opportunity.

IHS estimates that more than 20 billion cubic meters (Bcm) per year of shale gas production is possible in Germany by 2030, the equivalent of 25% of current consumption. Production would continue to rise after that, peaking at more than 25 Bcm in the mid 2030’s. Conventional and shale gas production would be almost 30 Bcm through the 2030s, enough to meet more than 35 % of current German gas demand. This volume would be similar to Germany’s current imports from Norway. Russian exports to Germany were 37 Bcm in 2013.

As I pointed out before, the UK green (and green finance) anti-narrative of inconsequential natural gas production needs to be updated, and it’s important here that IHS, who have a long and detailed experience of measuring the US shale revolution, believe – as I do about the UK (and France!) – that the potential gas resources are substantial.

Europe’s shale gas resources are material enough to make substantial differences in two key areas: cutting carbon emissions and cutting energy prices.

The European gas market is highly interconnected, and production in one market has an impact on prices in neighbouring markets. For this reason, IHS also undertook an analysis of overall European shale potential. Substantial production is possible in other countries, including Poland and the United Kingdom, if they adopt policies conducive to shale development. Total shale gas production in the EU28 could exceed 70 Bcm in 2030, increasing to almost 90 Bcm by 2040. This is on the same scale as current Norwegian pipeline exports to the EU of 100 Bcm. Russian exports to the EU in 2013 were 130 Bcm.

The European gas market is highly interconnected, and production in one market has an impact on prices in neighbouring markets. For this reason, IHS also undertook an analysis of overall European shale potential. Substantial production is possible in other countries, including Poland and the United Kingdom, if they adopt policies conducive to shale development. Total shale gas production in the EU28 could exceed 70 Bcm in 2030, increasing to almost 90 Bcm by 2040. This is on the same scale as current Norwegian pipeline exports to the EU of 100 Bcm. Russian exports to the EU in 2013 were 130 Bcm.

Development of local gas supply would put downward pressure on European prices, reducing them by as much as 20%

Production on this scale would have a clear impact on gas prices in the European market. Development of local gas supply would put downward pressure on European prices, reducing them by as much as 20% compared with a scenario in which Europe did not develop its shale endowment. At the same time, it would contribute to greater energy security, meeting an objective of both Germany and the European Union.

A switch from coal-fired power production to (shale) gas fired electricity would also contribute to lower CO2 emissions.

Bitter Enders

The energiewende is not dead. As I continuously try to point out to greens, gas is an “enabler” of renewables. Continuation on the current track will result in a decreasing role for gas over time, as domestic gas production declines and coal continues to dominate the thermal mix in Germany. The share of domestic gas production in Germany’s total gas consumption has decreased from 20% in 2000 to 10 % today. Increasing the role of indigenously produced gas in the power sector alongside mature renewables provides Germany with an opportunity to secure an affordable and sustainable path for the Energiewende.

The purist, Armaggedon narrative of some Bitter Enders of the Green movement will achieve from the edges exactly what the energiewende has so far achieved: absolutely nothing.

The IHS report, offers no less a hopeful vision than that of the energiewende. But most importantly, it offers an achievable one.

About the author

Nick Grealy is director of the energy consultancy No Hot Air, specialising in “public perception and acceptance issues of shale energy worldwide”. Describing himself as a “recovering energy consultant” who thinks the worst energy risk is getting talked into thinking you have one, he started following the shale energy revolution in 2008. First studying what he called at the time shale’s sudden emergence and future permanence he now studies shale’s impact worldwide across the energy spectrum. He has worked for private and public clients across Europe and is a frequent contributor to media while continuing to publish analysis of energy acceptance issues at www.nohotair.co.uk This article was first published on his website here and is republished with permission from the author. All rights reserved.

The IHS report claims that the energiewende is not delivering affordability and the chart shown appears to support this. In turn the argument is made to move to shale gas as a way of improving affordability.

As the DG ECFIN report published in Jan 2014 showed (part of the 2030 EC “package”), energy costs for much of German manufacturing industry are a very small (5.5% i.e. they spend much more on energy for a given unit of added value.

In the case of energy intensive industry the arguments put forward are generalised. Getting to specifics, I notice in 2012 that Norsk Hydro negotiated a good energy deal for its Neuss aluminium plant which led to an expansion of the plant. Same company is now expanding its Grevenbroich plant – just down the road. there are other examples – although I recognise that these may not fit well with the narrative on offer by both this writer and others. Or we could try Page 40 of the ECFIN report ”

“the EU-US goods balance has shown a persistent surplus for the EU withoutany clear sign of deterioration. Since the direct trade in goods constitutes one of the key indicators for assessing (changes in) competitiveness, one can tentatively conclude that the widening EU-US energy price gap has so far not visibly affected the EU industry’s market performance vis-a-vis theirs”

So the argument for shale gas as a way of reducing costs is valid but only if these costs are a) substantial b) having an impact. Given the above, neither seems to be the case. I notice that there is some resistance to new power lines in Germany – I’d suggest that this will pale into insignificance compared to what would happen if there was significant shale gas exploitation. Shale gas in Germany, in theory yes, in practise no.