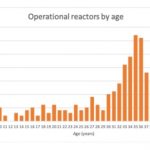

Denis Iurchak has taken a close look at nuclear decommissioning. Globally, 447 nuclear reactors are in operation as of January 2020. Of those, nearly 70% are older than 30 years (25% are older than 40 years). The IEA says around 200 commercial reactors are to be shut down in the next two decades. On top of that, 182 reactors are already in permanent shutdown. This means that between 200 and 400 reactors are likely to be decommissioned by 2040, … [Read more…]

Small nations have big plans for nuclear energy

Dan Yurman looks at how small nations are trying to increase their nuclear supply. Romania has the US and China both pitching for business. The Czech Republic is still vague about giving electricity price guarantees, something that caused the collapse of a $25bn nuclear tender in 2014. Ukraine looks at Small Modular Reactors. The author starts with the Baltics – net importers of electricity – and Estonia’s ambition to redress that balance using … [Read more…]